Making Relocations More Affordable for Employees

A recent report shows 78 percent of those surveyed associate home ownership with the American dream1, yet one in two Americans see housing affordability as a serious problem.2 What does this mean for companies who need to relocate their employees?

It’s an indicator that employees may be reluctant to relocate for several reasons:

- They want stability for their family, given the challenges of the last few years.

- Anxiety over rapidly rising inflation, higher housing costs and increased mortgage rates.

- Fear of moving to a higher cost of living area with many unknowns.

These are all real concerns. According to Fannie Mae, only 16 percent of U.S. consumers believe that now is a good time to buy a home. Another alarming statistic: mortgage applications in November 2022 fell by 25.2 percent compared to the previous year.3

Interest Rate Impact

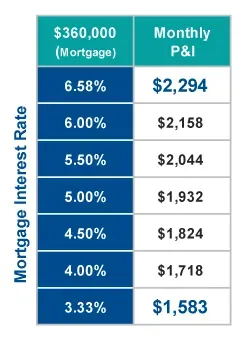

Last year, U.S. 30-year fixed mortgage rates had the biggest year-to-date rate increases in over 50 years. In January of 2022, the average rate was 3.33 percent – in January 2023 it was 6.58 percent!4 Negative buyer sentiment is often linked to mortgage rate increases.

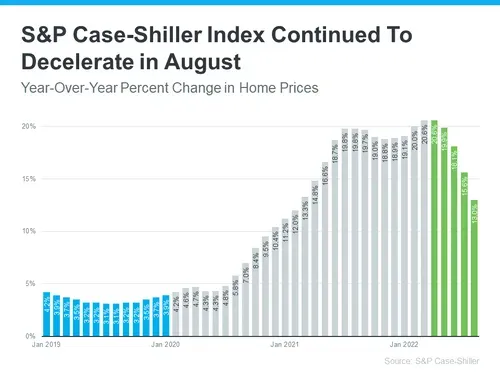

While today’s rates are historically low compared to the October 1981 peak of 18.45 percent, the escalation in home prices during the pandemic from mid-2021 to mid-2022 per the provided chart have greatly impacted employees’ concerns about relocating.

You can see why when you look at how a monthly mortgage for principal and interest has risen in one year. On a $360,000 30-year fixed mortgage (P&I), payments at the beginning of 2022 would have been $1,583 per month. By January of 2023, that same payment increased by $711 to $2,294!

Mortgage Rate Options to Consider

NEI helps client companies prepare for situations caused by market circumstances which are out of relocating employees’ control. Each company’s unique culture, budget, and drivers are taken into consideration when making suggestions to help retain talent while making your company attractive to new talent. Options to consider include:

Mortgage Interest Differential Allowance (MIDA)

MIDA programs were developed as a solution to assist employees when purchasing a home in the new location at a significantly higher interest rate. Popular options in the 1980s and 1990s, such MIDA policy benefits are getting dusted off again for consideration by some companies. As this benefit was rarely used over the last twenty years, any industry information or statistics are obsolete.

In this program, if a specific interest rate threshold is passed (e.g., 8 percent with at least 2 percent differential on the employee’s existing mortgage), the company would temporarily pay the difference in interest between the relocating employee’s former mortgage rate and their new one for a determined amount of time. The allowance is sent directly to the lender by the company and reflected on the employee’s payment.

Some companies require employees to invest their full equity from the sale of the old home into the purchase of the new home to be eligible. In addition, caps are sometimes placed on the total differential.

MIDAs can be difficult for companies from a budgeting perspective, however if the employee moves to a different home while the benefit is in effect, the coverage ceases and the company is no longer assisting.

3-2-1 Interest-Based Mortgage Subsidy

An appealing option for companies to consider is a subsidy program that supports mortgage payments over a set period of time to help the employee ease into the higher mortgage payment. Many companies use a three year period with the subsidized rate decreasing each year until the company would no longer be subsidizing interest. For budgeting purposes, some companies prefer to define a maximum subsidy dollar amount spent per year for the benefit.

Prepaid Interest

Companies can pay for loan discount points to assist relocating employees facing higher rates on a home purchase. Using a sliding scale, one point could equal one percent of a borrower’s mortgage and is interest that is paid upfront at closing. This lowers the rate for the life of the loan.

Some corporate mobility policies have a sliding scale for points coverage tied to the current market rate. If one uses a sliding scale, it may make sense to lower thresholds. Companies might offer to pay for one point when interest rates reach seven percent, two points at eight percent, and so forth. Thresholds help keep pace with changing mortgage environments and help make moving more agreeable.

Because this benefit impacts the life of the loan, this may not the best option for an employee who could be relocated again within a few years.

Unpredictable Markets and Economic Conditions

Prospective home buyers today face expensive ownership costs and prospective sellers contend with lower price expectations as well as unfavorable mortgage rates if buying again.

NEI constantly monitors market and economic conditions to proactively discuss various options with our clients that may assist them in adapting to meet volatile market challenges so recruitment and retention goals can be met.

For more information on the above programs or other needs, please reach out to your NEI representative. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Sources: 1) Mynd Consumer Insights Report; 2) Pew Research Center; 3) Fannie Mae; 4) Mortgage Bankers Association; 5) CNBC.

Making Relocations More Affordable for Employees

A recent report shows 78 percent of those surveyed associate home ownership with the American dream1, yet one in two Americans see housing affordability as a serious problem.2 What does this mean for companies who need to relocate their employees?

It’s an indicator that employees may be reluctant to relocate for several reasons:

- They want stability for their family, given the challenges of the last few years.

- Anxiety over rapidly rising inflation, higher housing costs and increased mortgage rates.

- Fear of moving to a higher cost of living area with many unknowns.

These are all real concerns. According to Fannie Mae, only 16 percent of U.S. consumers believe that now is a good time to buy a home. Another alarming statistic: mortgage applications in November 2022 fell by 25.2 percent compared to the previous year.3

Interest Rate Impact

Last year, U.S. 30-year fixed mortgage rates had the biggest year-to-date rate increases in over 50 years. In January of 2022, the average rate was 3.33 percent – in January 2023 it was 6.58 percent!4 Negative buyer sentiment is often linked to mortgage rate increases.

While today’s rates are historically low compared to the October 1981 peak of 18.45 percent, the escalation in home prices during the pandemic from mid-2021 to mid-2022 per the provided chart have greatly impacted employees’ concerns about relocating.

You can see why when you look at how a monthly mortgage for principal and interest has risen in one year. On a $360,000 30-year fixed mortgage (P&I), payments at the beginning of 2022 would have been $1,583 per month. By January of 2023, that same payment increased by $711 to $2,294!

Mortgage Rate Options to Consider

NEI helps client companies prepare for situations caused by market circumstances which are out of relocating employees’ control. Each company’s unique culture, budget, and drivers are taken into consideration when making suggestions to help retain talent while making your company attractive to new talent. Options to consider include:

Mortgage Interest Differential Allowance (MIDA)

MIDA programs were developed as a solution to assist employees when purchasing a home in the new location at a significantly higher interest rate. Popular options in the 1980s and 1990s, such MIDA policy benefits are getting dusted off again for consideration by some companies. As this benefit was rarely used over the last twenty years, any industry information or statistics are obsolete.

In this program, if a specific interest rate threshold is passed (e.g., 8 percent with at least 2 percent differential on the employee’s existing mortgage), the company would temporarily pay the difference in interest between the relocating employee’s former mortgage rate and their new one for a determined amount of time. The allowance is sent directly to the lender by the company and reflected on the employee’s payment.

Some companies require employees to invest their full equity from the sale of the old home into the purchase of the new home to be eligible. In addition, caps are sometimes placed on the total differential.

MIDAs can be difficult for companies from a budgeting perspective, however if the employee moves to a different home while the benefit is in effect, the coverage ceases and the company is no longer assisting.

3-2-1 Interest-Based Mortgage Subsidy

An appealing option for companies to consider is a subsidy program that supports mortgage payments over a set period of time to help the employee ease into the higher mortgage payment. Many companies use a three year period with the subsidized rate decreasing each year until the company would no longer be subsidizing interest. For budgeting purposes, some companies prefer to define a maximum subsidy dollar amount spent per year for the benefit.

Prepaid Interest

Companies can pay for loan discount points to assist relocating employees facing higher rates on a home purchase. Using a sliding scale, one point could equal one percent of a borrower’s mortgage and is interest that is paid upfront at closing. This lowers the rate for the life of the loan.

Some corporate mobility policies have a sliding scale for points coverage tied to the current market rate. If one uses a sliding scale, it may make sense to lower thresholds. Companies might offer to pay for one point when interest rates reach seven percent, two points at eight percent, and so forth. Thresholds help keep pace with changing mortgage environments and help make moving more agreeable.

Because this benefit impacts the life of the loan, this may not the best option for an employee who could be relocated again within a few years.

Unpredictable Markets and Economic Conditions

Prospective home buyers today face expensive ownership costs and prospective sellers contend with lower price expectations as well as unfavorable mortgage rates if buying again.

NEI constantly monitors market and economic conditions to proactively discuss various options with our clients that may assist them in adapting to meet volatile market challenges so recruitment and retention goals can be met.

For more information on the above programs or other needs, please reach out to your NEI representative. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Sources: 1) Mynd Consumer Insights Report; 2) Pew Research Center; 3) Fannie Mae; 4) Mortgage Bankers Association; 5) CNBC.

Making Relocations More Affordable for Employees

A recent report shows 78 percent of those surveyed associate home ownership with the American dream1, yet one in two Americans see housing affordability as a serious problem.2 What does this mean for companies who need to relocate their employees?

It’s an indicator that employees may be reluctant to relocate for several reasons:

- They want stability for their family, given the challenges of the last few years.

- Anxiety over rapidly rising inflation, higher housing costs and increased mortgage rates.

- Fear of moving to a higher cost of living area with many unknowns.

These are all real concerns. According to Fannie Mae, only 16 percent of U.S. consumers believe that now is a good time to buy a home. Another alarming statistic: mortgage applications in November 2022 fell by 25.2 percent compared to the previous year.3

Interest Rate Impact

Last year, U.S. 30-year fixed mortgage rates had the biggest year-to-date rate increases in over 50 years. In January of 2022, the average rate was 3.33 percent – in January 2023 it was 6.58 percent!4 Negative buyer sentiment is often linked to mortgage rate increases.

While today’s rates are historically low compared to the October 1981 peak of 18.45 percent, the escalation in home prices during the pandemic from mid-2021 to mid-2022 per the provided chart have greatly impacted employees’ concerns about relocating.

You can see why when you look at how a monthly mortgage for principal and interest has risen in one year. On a $360,000 30-year fixed mortgage (P&I), payments at the beginning of 2022 would have been $1,583 per month. By January of 2023, that same payment increased by $711 to $2,294!

Mortgage Rate Options to Consider

NEI helps client companies prepare for situations caused by market circumstances which are out of relocating employees’ control. Each company’s unique culture, budget, and drivers are taken into consideration when making suggestions to help retain talent while making your company attractive to new talent. Options to consider include:

Mortgage Interest Differential Allowance (MIDA)

MIDA programs were developed as a solution to assist employees when purchasing a home in the new location at a significantly higher interest rate. Popular options in the 1980s and 1990s, such MIDA policy benefits are getting dusted off again for consideration by some companies. As this benefit was rarely used over the last twenty years, any industry information or statistics are obsolete.

In this program, if a specific interest rate threshold is passed (e.g., 8 percent with at least 2 percent differential on the employee’s existing mortgage), the company would temporarily pay the difference in interest between the relocating employee’s former mortgage rate and their new one for a determined amount of time. The allowance is sent directly to the lender by the company and reflected on the employee’s payment.

Some companies require employees to invest their full equity from the sale of the old home into the purchase of the new home to be eligible. In addition, caps are sometimes placed on the total differential.

MIDAs can be difficult for companies from a budgeting perspective, however if the employee moves to a different home while the benefit is in effect, the coverage ceases and the company is no longer assisting.

3-2-1 Interest-Based Mortgage Subsidy

An appealing option for companies to consider is a subsidy program that supports mortgage payments over a set period of time to help the employee ease into the higher mortgage payment. Many companies use a three year period with the subsidized rate decreasing each year until the company would no longer be subsidizing interest. For budgeting purposes, some companies prefer to define a maximum subsidy dollar amount spent per year for the benefit.

Prepaid Interest

Companies can pay for loan discount points to assist relocating employees facing higher rates on a home purchase. Using a sliding scale, one point could equal one percent of a borrower’s mortgage and is interest that is paid upfront at closing. This lowers the rate for the life of the loan.

Some corporate mobility policies have a sliding scale for points coverage tied to the current market rate. If one uses a sliding scale, it may make sense to lower thresholds. Companies might offer to pay for one point when interest rates reach seven percent, two points at eight percent, and so forth. Thresholds help keep pace with changing mortgage environments and help make moving more agreeable.

Because this benefit impacts the life of the loan, this may not the best option for an employee who could be relocated again within a few years.

Unpredictable Markets and Economic Conditions

Prospective home buyers today face expensive ownership costs and prospective sellers contend with lower price expectations as well as unfavorable mortgage rates if buying again.

NEI constantly monitors market and economic conditions to proactively discuss various options with our clients that may assist them in adapting to meet volatile market challenges so recruitment and retention goals can be met.

For more information on the above programs or other needs, please reach out to your NEI representative. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction.

Sources: 1) Mynd Consumer Insights Report; 2) Pew Research Center; 3) Fannie Mae; 4) Mortgage Bankers Association; 5) CNBC.